Director of Product hired to lead the hyper-growth phase. Oversaw the consumer app, shaping a product that is synonymous with P2P transfers.

Date: 06.2018 – 10.2019

Results

9-figure revenue growth

Wrote and implemented the Instant Transfer strategy, generating exponential revenue growth in year one

8-figure savings

Identified and implemented payment optimizations that delivered massive cost savings

7-figure monthly user growth

Fueled the consumer app growth phase by ensuring a seamless and delightful experience

- 01100% Net New Actives

- 02Revenue growth strategy

- 03Recipient verification

- 04Optimizing Plaid

- 05Launching RTP

- 06Reimagining the UX

- 07Shipping on time and early

Problem

In an era of hyper-growth, FinCEN regulations threatened our most important metric: NNA.

Scaling to millions of monthly new users: How we stayed compliant and kept growing

Problem

In an era of hyper-growth, FinCEN regulations threatened our most important metric: NNA.

Solution

When I joined Venmo in 2018, we faced a significant regulatory challenge from FinCEN, part of the U.S. Treasury. FinCEN required Venmo to implement a Customer Identification Program (CIP) to verify users’ identities before they could send money from their balance accounts. However, introducing identity verification at the point of enrollment posed a major risk to our most critical growth metric, Net New Actives (NNA), which had established Venmo as the most widely used P2P payment platform in the U.S.

To address this, we developed a CIP platform that allowed us to decouple the processes of holding and sending money. New users would receive money into their Venmo balance accounts without undergoing immediate verification. When they sent money, however, we pulled funds directly from their linked bank accounts instead of their Venmo balance until verification was completed. This solution required a complete re-architecture of Venmo’s foundational money movement system, a significant technical overhaul since the platform’s inception.

By implementing this strategy, we maintained our core metric of 100% NNA user growth while meeting FinCEN’s regulatory requirements. This achievement was made possible by an exceptional team who made difficult decisions to reprioritize the roadmap, reallocate resources, and work tirelessly to deliver this transformative solution within tight deadlines.

- 01100% Net New Actives

- 02Revenue growth strategy

- 03Recipient verification

- 04Optimizing Plaid

- 05Launching RTP

- 06Reimagining the UX

- 07Shipping on time and early

Problem

Venmo was founded with the belief that money movement should be free for consumers. Our challenge from leadership was to drive 9-figure revenue growth without sacrificing our core values and product accessibility.

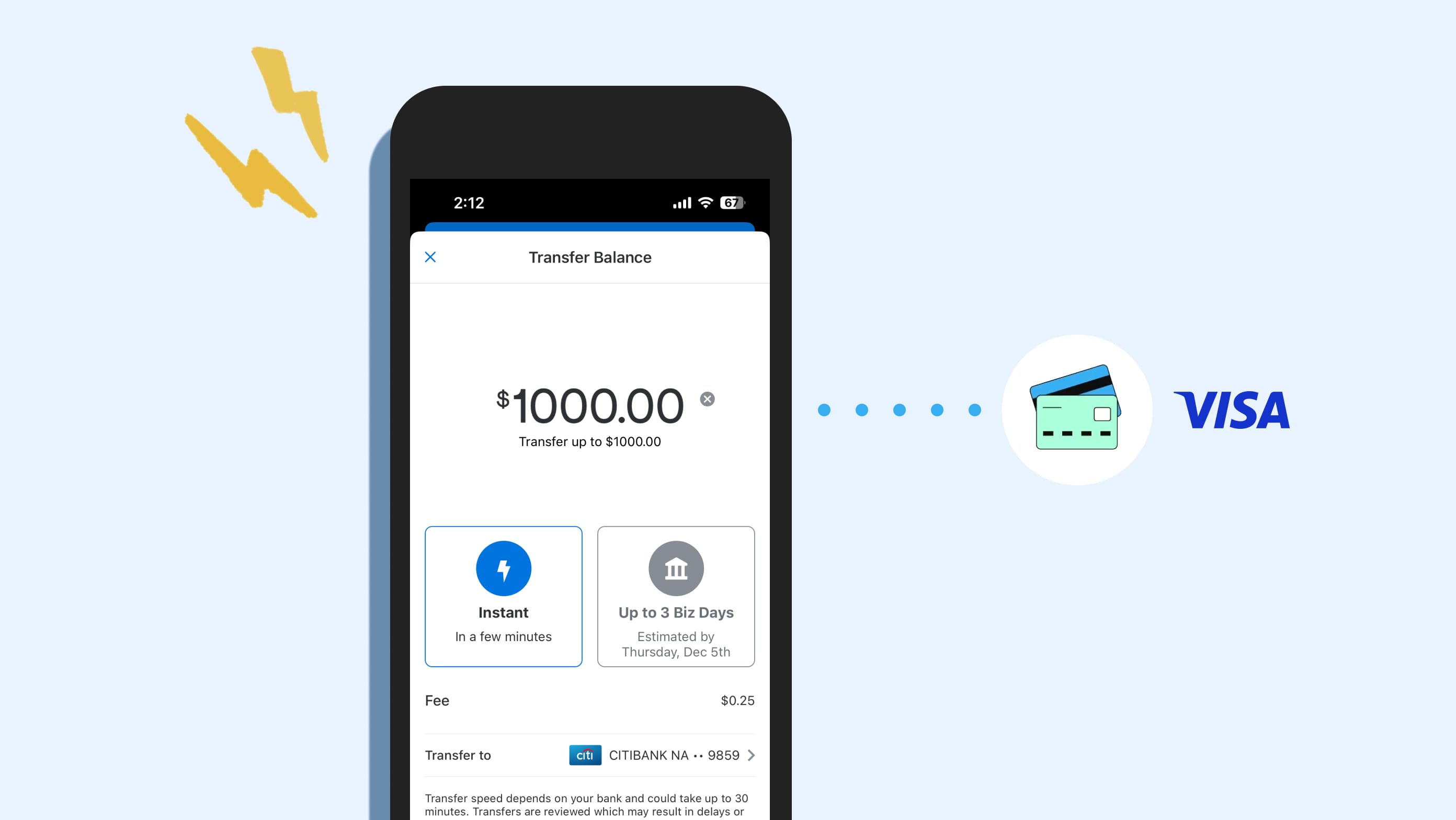

Our journey to 9-figure revenue growth in year one

Problem

Venmo was founded with the belief that money movement should be free for consumers. Our challenge from leadership was to drive 9-figure revenue growth without sacrificing our core values and product accessibility.

Solution

In 2018, with user growth skyrocketing, there was a need to have revenue keep pace. Instant Transfers were a relatively new feature powered by Visa Direct OCT rails. After exploring numerous revenue growth initiatives, we identified that scaling revenue would require adjusting our pricing model. This involved moving from a flat $0.25 fee to a percentage-based fee of 1% per Instant Transfer. Through detailed financial modeling and intense internal discussions, we carefully weighed the implications on our brand identity, particularly considering Zelle’s free instant transfers and Cash App’s 1% pricing.

Ultimately, we implemented a 1% fee with a $10 cap, successfully restructured our pricing, and rolled it out to customers. This change not only drove substantial revenue growth but also exceeded our first-year projections, all while experiencing lower-than-expected churn.

- 01100% Net New Actives

- 02Revenue growth strategy

- 03Recipient verification

- 04Optimizing Plaid

- 05Launching RTP

- 06Reimagining the UX

- 07Shipping on time and early

Problem

We needed to address the rise in customer complaint volume for sending money to the wrong recipient. P2P transfers without end-user verification opened us up to fraud and customer appeasement, creating thousands of support tickets and excessive operational overhead.

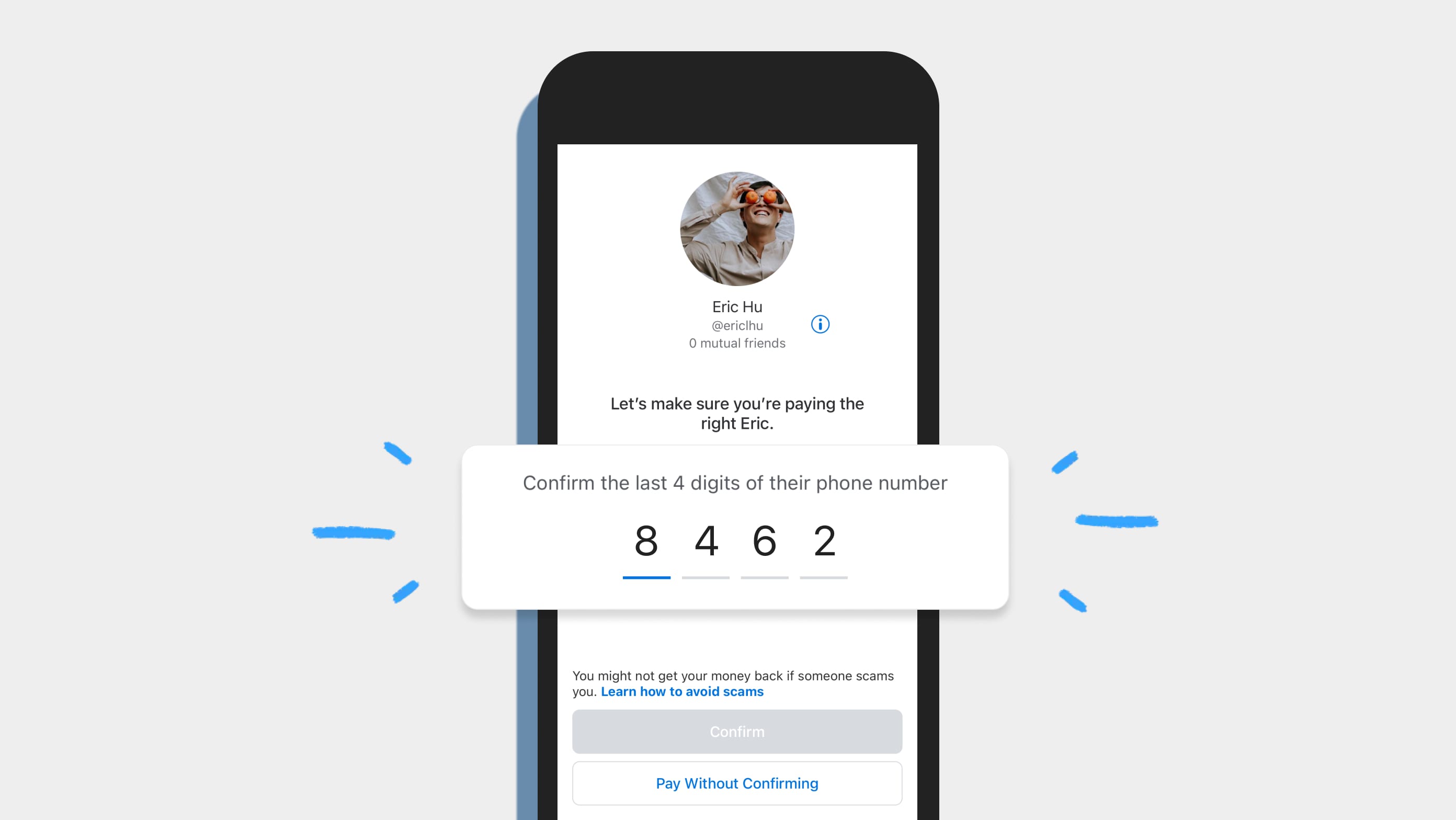

Creating an improved new recipient sending experience that reduced fraud and customer appeasements

Problem

We needed to address the rise in customer complaint volume for sending money to the wrong recipient. P2P transfers without end-user verification opened us up to fraud and customer appeasement, creating thousands of support tickets and excessive operational overhead.

Solution

Customers often sent money to the wrong person during initial transactions, especially when they were not physically near each other. This issue created a frustrating customer experience, leading to consistently high volumes of customer service tickets. These errors resulted in increased operational costs, wasted man-hours, and opened opportunities for fraud. After analyzing thousands of support cases, we identified a clear pattern: Venmo usernames were frequently mistyped, causing payments to be sent to unintended recipients.

To address this, we implemented a solution requiring users to confirm the last four digits of the recipient’s phone number when sending money to someone for the first time. While this approach initially faced resistance due to Venmo’s core principle of minimizing friction, it ultimately introduced a new layer of confidence and security. Although it added a minor “speed bump” to the process, users appreciated the added assurance, and it significantly reduced errors.

In the first quarter following this release, the results were compelling: erroneous payments decreased by 25%, and customer service inquiries dropped by 30%. This solution not only improved user experience but also reduced operational strain and costs, aligning with our commitment to seamless, reliable transactions.

- 01100% Net New Actives

- 02Revenue growth strategy

- 03Recipient verification

- 04Optimizing Plaid

- 05Launching RTP

- 06Reimagining the UX

- 07Shipping on time and early

Problem

Rapid user growth led us to have a large rise in back-end costs associated with customers looking to authenticate and pay directly with their bank account.

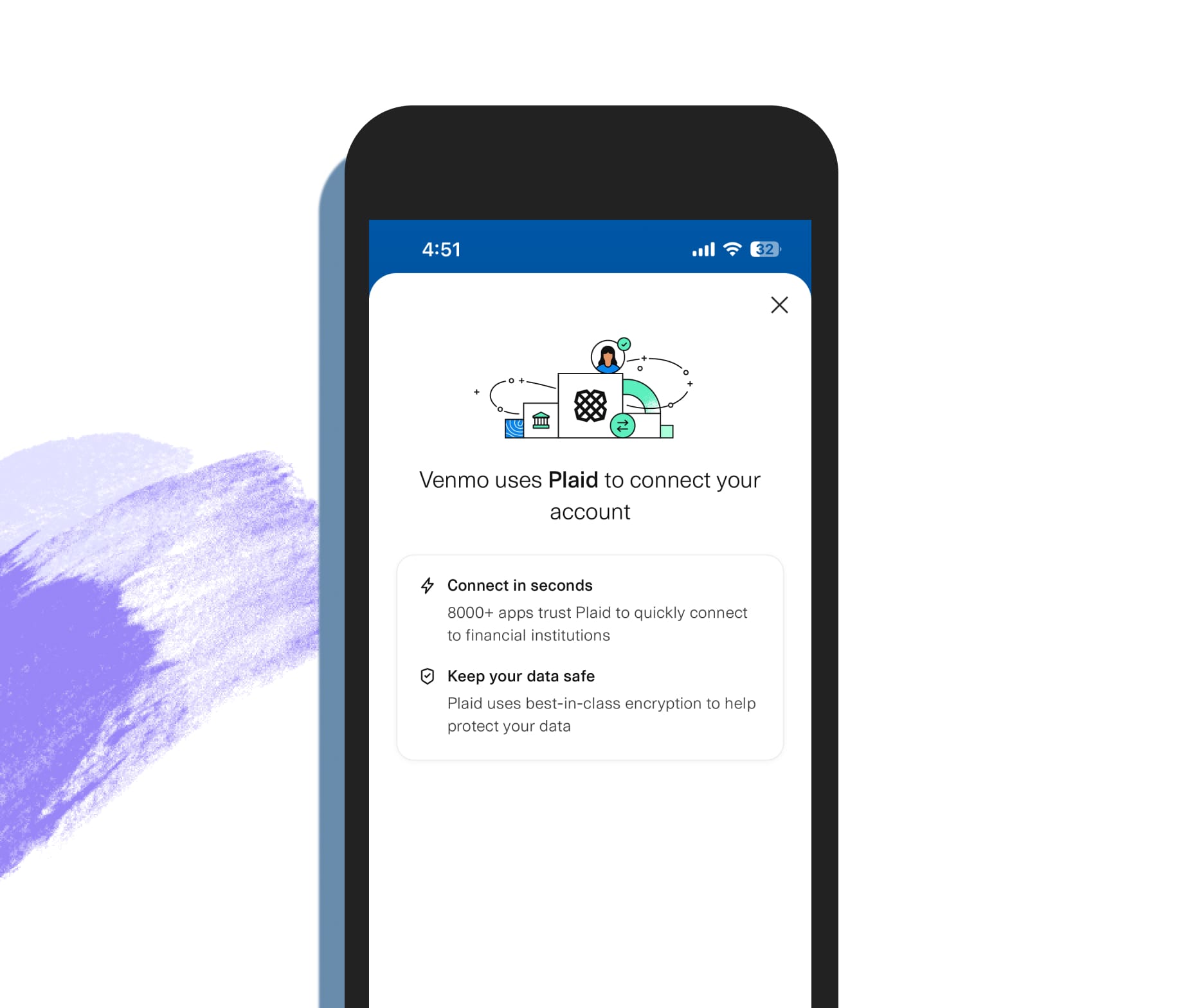

Identifying an opportunity to streamline customer authentication and reduce Plaid fees

Problem

Rapid user growth led us to have a large rise in back-end costs associated with customers looking to authenticate and pay directly with their bank account.

Solution

During our rapid growth phase, Venmo was experiencing rising costs associated with its Plaid integration. We enjoyed the partnership, especially with such an exceptional product-led company, but we needed a better way to leverage the Plaid portfolio to enable streamlined "pay with bank" services.

Upon reviewing our budget, we discovered two key issues: we were paying for features we didn’t fully utilize, and we experienced a disproportionately high disconnect rate with certain banks. These bank disconnects not only disrupted the customer experience but also caused users to default to paying with debit cards, increasing costs due to higher processing fees on debit rails.

By analyzing the data in detail, we optimized the Plaid integration and developed an internal white-labeled fraud monitoring system. This system tracked customer behavior and proactively mitigated disconnects for our most reliable users, ensuring they could seamlessly transact using their already connected bank accounts. This enhancement improved the overall user experience while reducing reliance on costly alternatives. In the first year alone, these efforts resulted in a 7-figure cost savings, showcasing the value of strategic optimization and proactive problem solving.

- 01100% Net New Actives

- 02Revenue growth strategy

- 03Recipient verification

- 04Optimizing Plaid

- 05Launching RTP

- 06Reimagining the UX

- 07Shipping on time and early

Problem

We needed to reduce payment processing fees while maintaining our exceptional user experience with Instant Transfers.

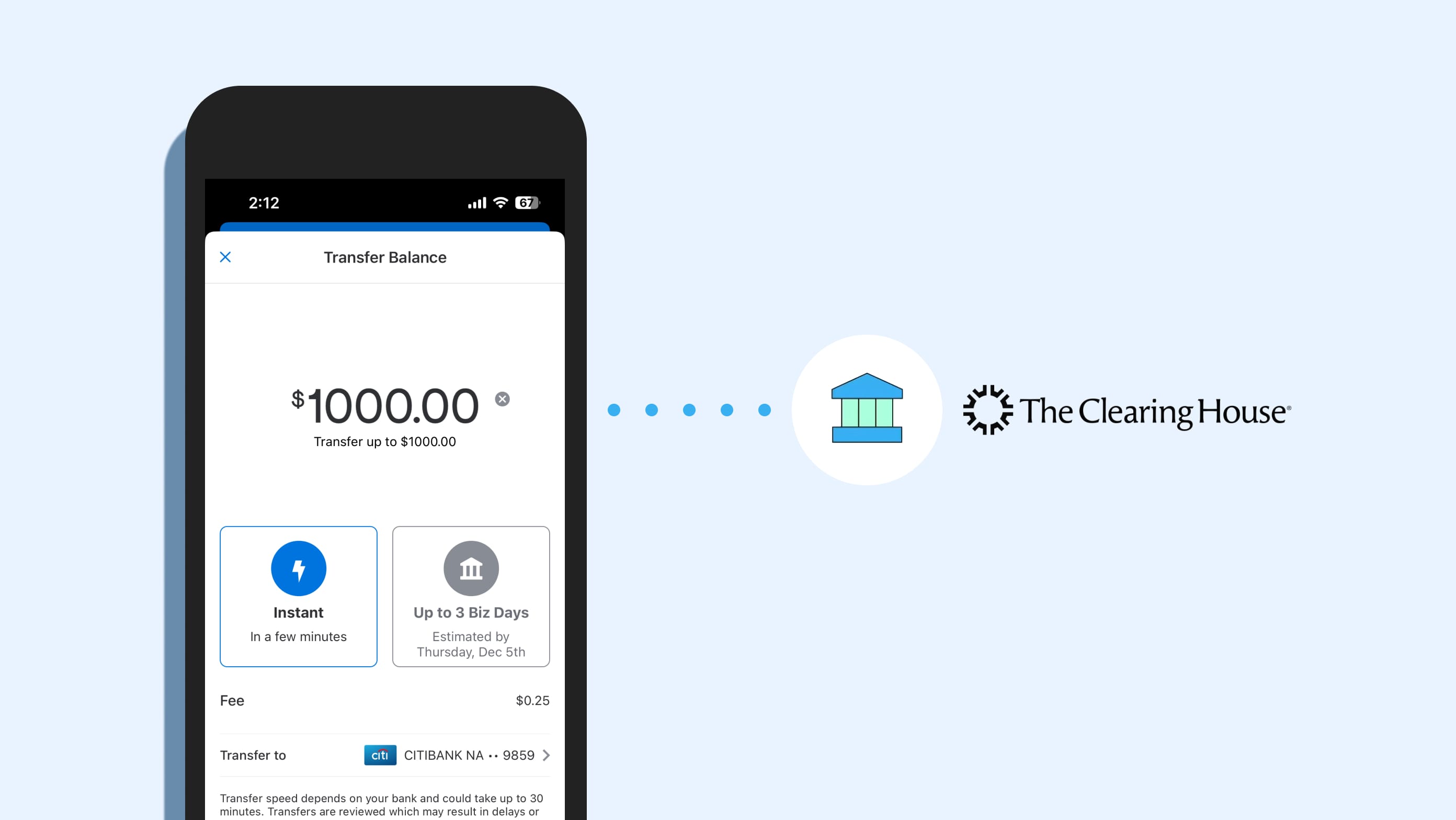

Real-time payments: How we hit $100M in 30 days

Problem

We needed to reduce payment processing fees while maintaining our exceptional user experience with Instant Transfers.

Solution

Successfully rolling out Visa Direct drove our Instant Transfer revenue growth strategy, but not every customer used a debit card for payments. Standard transfers via ACH still took an average of two days to process, leaving many customers frustrated by the lack of speed. Meeting customer expectations for faster transactions while optimizing costs became a top priority.

Recognizing the emergence of real-time payments (RTP) in the market, we partnered with JPMorgan and The Clearing House to implement RTP for all customers linked through their bank accounts. This solution enabled instant transfers for a broader customer base, providing the speed they desired while significantly reducing processing costs.

The rollout exceeded expectations, with $100M in payment volume processed within the first 30 days. Additionally, the optimization delivered 8-figure annual cost savings, directly enhancing our bottom line and reinforcing our commitment to a seamless, efficient user experience.

- 01100% Net New Actives

- 02Revenue growth strategy

- 03Recipient verification

- 04Optimizing Plaid

- 05Launching RTP

- 06Reimagining the UX

- 07Shipping on time and early

Problem

How do we modernize a beloved product without alienating existing users?

Reimagining the iOS and Android apps to deliver a consistent, unified experience across platforms

Problem

How do we modernize a beloved product without alienating existing users?

Solution

With Venmo’s meteoric growth, the end-to-end user experience across iOS and Android had started to show its age, becoming inconsistent between platforms. Meanwhile, the web experience, once a key entry point, had largely fallen by the wayside, with minimal usage and support. These gaps extended to the backend where inconsistent APIs were slowing down development cycles.

The challenges were clear: the home feed alone had 23 distinct differences across platforms, and the signup flow spanned a cumbersome 18 screens. Users were navigating a disjointed experience that no longer aligned with their expectations or Venmo’s brand promise.

Fueled by deep user research, we reimagined the most common user journeys, from signup to sending money, and charted a completely new, cohesive UX for iOS and Android. Simultaneously, we made the strategic decision to sunset the web experience, focusing our efforts on delivering a streamlined and modern mobile-first experience. This transformation set the stage for a unified, intuitive platform that reinforced Venmo’s commitment to simplicity and innovation.

- 01100% Net New Actives

- 02Revenue growth strategy

- 03Recipient verification

- 04Optimizing Plaid

- 05Launching RTP

- 06Reimagining the UX

- 07Shipping on time and early

Problem

Rapid growth and not enough people were causing our product delivery to fall behind. We needed a new approach to fix our delivery times to keep up with customer demand.

Designing a refined software development process to standardize on-time product delivery

Problem

Rapid growth and not enough people were causing our product delivery to fall behind. We needed a new approach to fix our delivery times to keep up with customer demand.

Solution

Joining Venmo to lead the consumer P2P app, I inherited a critical challenge: product delivery was falling behind despite rapid growth. With no immediate budget for team expansion, I needed to improve productivity using existing resources. My team was responsible for the core app including registration, P2P transfers, the social feed, balances, and settings.

After diving in, I discovered the root cause: while the team was committed to agile principles, unclear requirements and constant revisions were creating inefficiencies that disrupted engineering planning. To address this, I introduced a refined process for defining requirements and writing user stories, incorporating specific stage gates to ensure clarity before work began. This allowed engineers to better assess scope and size tasks.

Within six months, the new process provided end-to-end visibility into development workflows while maintaining agile flexibility. Releases began consistently meeting or beating deadlines, proving we could operate efficiently as a lean team despite Venmo's rapid growth.

“Where there’s ambiguity, you’ll find Abe doing his best work.”

—Ben Mills VP Product